Bumble (BMBL): Why The Stock Is Definitely A Swipe Left

Bumble (BMBL): Why The Stock Is Definitely A Swipe Left

Bumble Stock Full Valuation: Discounted Cash Flow And Price Forecast.

Subscribe to get the next intrinsic valuation straight to your inbox! 👇

Fundamental analysis, discounted cash flow, sensitivity and scenario analysis, etc.

DISCLAIMER: The publication expresses my own opinions. Information presented is for educational purposes ONLY and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies.

Introduction

Bumble (Nasdaq:BMBL) came to the centre of attention for two reasons:

The initial public offering (IPO), where the company raised $ 2.2bn from investors at $43 a share.

The last earning report, where Bumble reported $165.6 million in revenues versus an expected value of $163.3 million.

Bumble Investment thesis

According to my analysis, Bumble (NASDAQ:BMBL) is highly overvalued. To justify the current valuation, the company will need to grow with a compounded annual growth rate of over 35% and reach a 30% operating margin.

These expectations are too high, considering that the company only has a minimal competitive advantage and that the market doesn't have any barriers to entry. I expect Bumble's fair value to be around $20.50, 66% lower than the actual price.

The story behind the numbers

According to Match Group's (NASDAQ:MTCH) most recent 10-K:

As more internet-connected singles utilize online dating products and the stigma around dating continues to erode, there is a huge potential for accelerating growth in the use of dating products globally.

I believe that Bumble is well set to ride the online dating trend, but I don't expect it to substantially increase its market share after the fifth year.

Bumble competitive advantage

Bumble is a dating app very similar to Tinder and the rest of the dating apps. The app shows you a series of profile, and you swipe right if you like the person or left if you don't. If you like each other, then it's a match, and you can start talking. But with Bumble, there is a catch: Only women can start the conversation.

With this simple rule, the company is trying to create its own competitive advantage by pursuing a differentiation-focus strategy: building a women-centred dating app. In its most recent 10-K, Bumble wrote:

Our users connect deeply with our brand, making it a powerful marketing tool which generates word of mouth virality and strong, efficient user acquisition.

While I believe that enhance the brand through marketing campaigns centred around women is an excellent idea, I don't think it will be enough to succeed in the dating industry. The addressable market is too broad and could easily be targeted by more specific dating apps aimed at, for example, older age groups (Lumen and SilverSingle for over 50) or specific religion (Muzmatch.com for Muslims or JDate for Jewish persons).

In addition, the concept of "swiping" is getting old, and it's being replaced by more meaningful ways of matching already offered by the new apps such as Hinge or Once.

Bumble's competitors

When you open the app store, you may see a long list of dating apps, but most of them are owned by the same company, Match Group. The group owns a huge portfolio of brands, including Tinder, Match, OkCupid and Hinge. This makes Match the biggest direct competitor of Bumble.

Even if pursuing a differentiation focus strategy is a great idea, what makes a difference in a dating app is the number of active users (network effect). Match is clearly winning in both the number of users and paying subscribers. Last year Bumble only added 500,000 new paying subscribers (+25%), while Match increased its paying users by 1,147,000 (+12%). In addition, the company has never succeeded in being a disruptive force, and its growth has been lagging behind that of other, less famous apps.

Source: Match Group business overview March 2021

Fundamental Analysis

In the last fiscal year, Bumble reported $ 582.18m in revenue (19% y/y growth), an operating profit of $ 32.63m and an operating margin of 5.6%, down from 19.1% last year.

The gross profit margin has been stable at around 70-73% for the past 3 years.

The consensus estimates reported by Capital IQ provide a revenue growth rate of 24% for the next 3 year and an operating margin of 19.64% in 2023.

Vertical analysis

1] Direct competitor

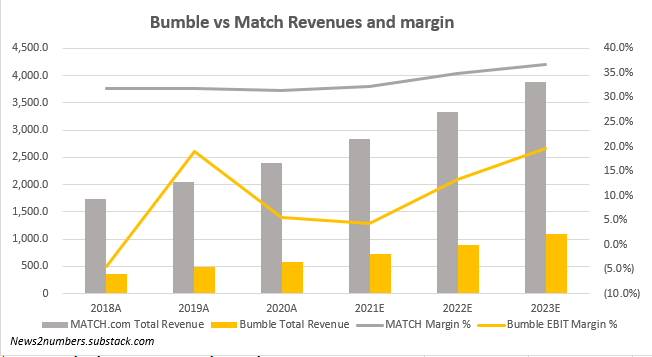

The Match Group (MTCH), Bumble’s direct competitor, increased its revenues (+16.6%) and operating profits in 2020.

The group’s EBIT margin stayed stable at 34% and is expected to remain stable in the next 3 years.

Bumble is expected to grow faster than Match in the next 3 years but with a lower operating margin. (34% Match vs 19% Bumble)

2] Interactive media and services industry

Bumble and the rest of the dating apps belong to the interactive media and services industry.

How is Bumble performing compared to the industry?

In red, I highlighted the percentile where Bumble stands.

The company has an EBIT margin within the 5th percentile, just below the industry’s media, but has a Return on Invested Capital and a Sales to IC ratio in the lowest percentiles.

The reason behind the low ROIC and capital turnover is the acquisition of Worldwide Vision Limited on the 29th of January 2020. This added to their balance sheet:

Goodwills for $ 1,455m;

Intangibles for $ 1,785m including $ 1,430 for the brand.

How much is Bumble (BMBL) worth?

1] Revenue growth.

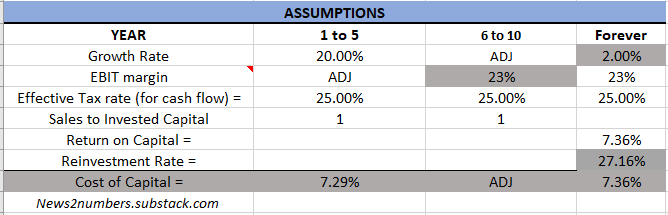

I expect a revenue growth rate of 20% for the next five years to reflect the overall online dating market's growth and increase in market share.

The growth rate will progressively slow down towards the risk-free rate in year 10.

2] Operating (EBIT) margin growing towards 23% in year 5.

I expect Bumble to move towards an EBIT margin of 23%, the 8th industry percentile.

It’s lower than its direct competitor, Match Group, but since Bumble has and will have a lower user base, the acquisition costs will be higher.

3] Global tax rate of 25%: the business expands worldwide, hence a global tax rate.

4] Marginal Sales to Invested Capital ratio of 1.

I expect Bumble to reinvest with a sales to capital ratio of 1, the industry median.

5] Cost of Capital of 7.29% for the years 1 to 5, slowly adjusting to 7.36% on year 10.

The increase in the cost of capital is due to the expected increase in the risk-free rate to 2% after year 5 to reflect an increase in inflation.

An equity risk premium of 6% to reflect global operations;

A beta of 1;

Default spread of 4.03% based on the B rating.

The cells in grey contain a formula:

Growth rate terminal year = risk-free rate;

EBIT Margin years 6-10 equal to terminal year;

Reinvestment rate terminal year = Growth rate / Return on capital.

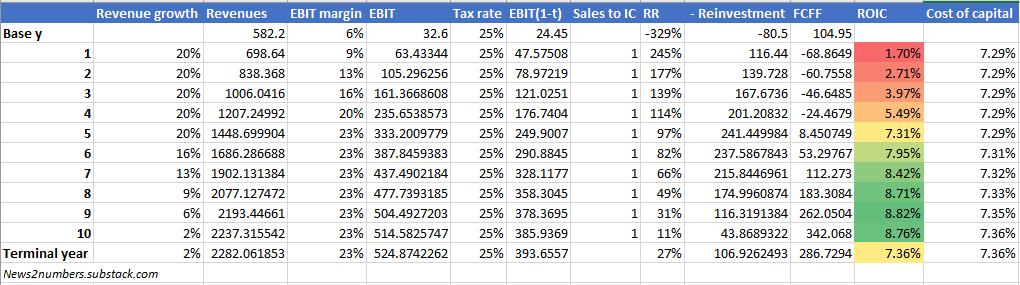

Bumble Free Cash Flow

Chart:

The Return on Invested Capital will peak at 8.82% in year 9 and decrease to the cost of capital in the terminal year.

I don’t see any sustainable moat around Bumble’s business to give it a higher return than its cost of capital after year 10.

Bumble’s fair value

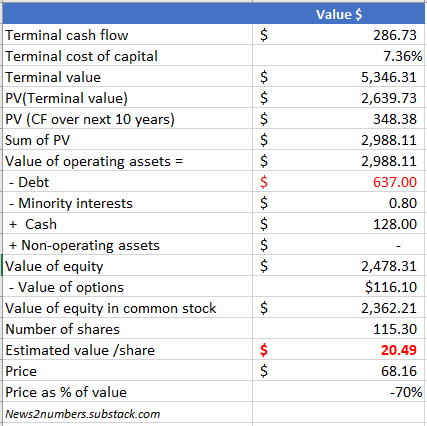

Summing up the present value of all the future cash flows, taking out debt, minority interest, and adding cash, we get a fair value for the Bumble shares of $ 20.49.

Even if on the balance sheet the outstanding debt is $ 827m, the company wrote on its 10-k that it would use its IPO proceed to repay $ 200m of the existing debt, so I only added $ 637m of debt.

The rest of the IPO proceeds will be used “to purchase or redeem an equivalent aggregate number of shares of Class A Common Stock and Common Units from certain entities affiliated with The Blackstone Group Inc.”. As a result, the $ 1.991m won’t be added to the valuation.

According to my valuation, Bumble is overvalued by 70%.

The value created by future growth is 85% of the total value. This definitely makes Bumble a growth company.

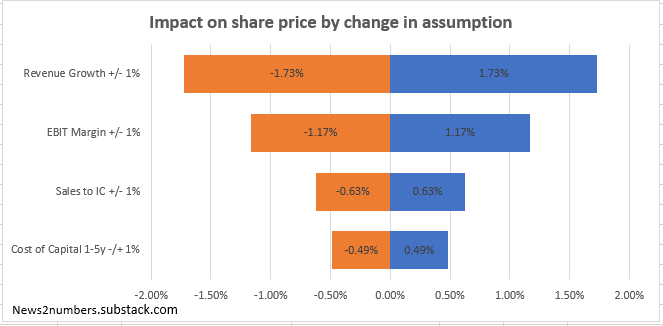

What are the main factors driving Bumble’s value?

By performing a sensitivity analysis, I get that the fair value of Bumble is mainly driven by a change in the expected growth rate and EBIT margin.

A percentage rise of 1% in the growth rate (e.g. from 20% to 20.2%, not to 21%) increases the fair value by 1.73%, while the same increase in the EBIT margin would cause a rise of 1.17%.

On the other side, a 1% increase in the Sales to IC ratio or cost of capital produces a much smaller effect on the underlying value.

What does the market expect from Bumble?

To understand the market expectations for Bumble, I ran a scenario analysis of the two main inputs: growth rate and operating margin.

The current price of $ 68.16 would be justified by a compounded annual growth rate of over 35% combined with a very high operating margin (30% +).

Bumble Montecarlo analysis

As John Maynard Keynes once said:

“It is better to be roughly right than precisely wrong”.

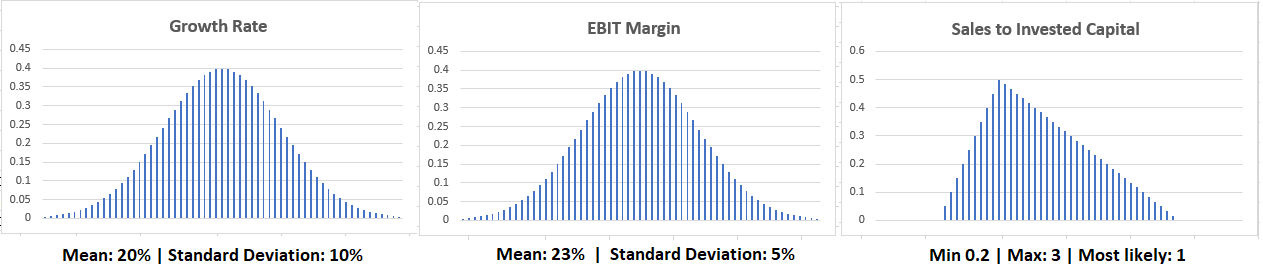

For this reason, instead of focusing only on single, static assumptions, I like to integrate the intrinsic valuation with a Montecarlo analysis.

Instead of using a single value for each input, I’ll use a random distribution of values and check the frequency/probability of each fair value.

Distribution of values:

Growth rate: normal distribution with mean 20% and standard deviation of 10%.

66% of the value will be within 10% and 30% growth rate.EBIT Margin: normal distribution with mean 23% and standard deviation of 5%.

Sales to IC: triangular distribution. Minimum value 0.2, maximum 1 and most likely 1.

After 1000 trials, I get a lognormal distribution with a mean of $26.76 and a median of $22.50.

According to the Monte Carlo simulation, at the current price of $ 68.18, Bumble has only a 7.4% probability of being undervalued / a good buy.

The 25th percentile is $ 12.37, and the 75th at $ 37.01.

Short catalyst

To close the gap between the fair value and the price, the stock needs a catalyst that forces the investors to reassess their expectations. In my opinion, the catalyst will arrive as soon as Bumble reports lower than expected user growth or operating margin, and this could happen at any upcoming earnings report.

Until that point, the stock could keep performing well while riding the tech stock mania. As a result, any short position should be placed with instruments with limited risk as put options, rather than directly shorting the stock.

Conclusion

I believe that Bumble is highly overpriced like most of the tech stocks right now. I'm convinced that the small probability of being fairly valued represents a good short play as soon as the company starts missing growth expectations.

Subscribe to get the next intrinsic valuation straight to your inbox! 👇

Fundamental analysis, discounted cash flow, sensitivity and scenario analysis, etc.