Robinhood: intrinsic valuation, risks and opportunities.

Robinhood: intrinsic valuation, risks and opportunities.

At which price Robinhood should be trading? (Nasdaq:HOOD)

When is the best time to buy stocks? When they are CHEAP!

Subscribe to get the next Discounted Cash Flow valuation straight to your inbox! 👇

DISCLAIMER: The publication expresses my own opinions. Information presented is for educational purposes ONLY and does not intend to make an offer or solicitation to sell or purchase any specific securities, investments, or investment strategies.

Introduction

RobinHood and the rest of the brokerage industry are living their best moment ever. Bored unemployed people with plenty of new benefits in their bank account flooded the online brokers to get fun and make some money.

The Bitcoin&DogeCoin saga, together with WallStreetBet’s short squeezes, made the new traders feel powerful, and, as a consequence, it pushed trading mania towards its extreme.

Brokers worldwide are making plenty of revenues, but I don’t believe this level of irrational exuberance will continue much longer. The revenue levels they generated will soon revert to the mean, either due to new regulations or lower interest in the stock market.

In this article, I will analyse the threats and opportunities ahead for Robinhood and translate them into a fair value estimation using the Excess Return Model.

Robinhood S.W.O.T. analysis

The biggest Robinhood’s strength is its zero commission and extremely easy and user-friendly platform, which appeals to the wanna-be-Wolf-of-Wall-Street kind of traders. These investors are the perfect business for Robinhood because they trade a lot, lose their funds, deposit and start again.

On the other side, its biggest strength is also its bigger weakness. Robinhood’s clients trade more but with smaller amounts and, since they generally lose, the company needs to rely on a constant flow of new deposits. In addition, they will also find problems diversifying its primary source of revenue, the payment for order flow, with other products. Retails traders just want to trade the last trendy stocks at the lowest cost. They are not interested in mutual funds, pensions plans, etc.

Thanks to the brand awareness generated with the short squeezes of the meme stocks, the headlines about the payment for order flow (PFOF) and the recent IPO, Robinhood has the opportunity to expand quickly in other countries with the minimum marketing effort. Everyone knows Robinhood and, in case they succeed to expand in other countries, plenty of traders will register and deposit. Even just to check how the famous app works.

At the same time, there is one significant threat to the future of Robinhood (and his brother Coinbase): regulation.

Robinhood’s mission is to democratise finance for all. However, what it really did was allowing the most financially illiterate people to access the financial markets and start gambling as they were doing with the lottery. The regulators will realise that and begin to add new rules on either the marketing, the instruments allowed or the payment for order flow. If this happens, Robinhood will rapidly lose its primary source of income and need to start charging commission or changing commercial strategy.

RobinHood Fundamental analysis

The company was growing fast and succeeded to close the fiscal year 2020 with a profit. However, considering the past 6 months of 2021, Robinhood lost over $ 2bn in the last 12 months. The main reason is the charge for change in the Fair Value of Convertible Notes and Warrant Liability of over $ 2bn.

Although it may be considered a one-off charge and all the convertible notes have been converted to equity at the IPO, I don’t like to exclude it because it’s part of their cost of debt. If Robinhood needs to add plenty of “sweeteners” (warrants, etc.) to their issuances, it means that no one wants to lend them money with standard conditions. It’s either the warrants or a high interest rate, and in the latter, it would have shown in the continuous operations.

Robinhood’s direct competitors are Charles Schwab (now including TD Ameritrade) and Interactive Broker (IBKR). Looking at the past 10 years, TD Ameritrade is the top performer in terms of ROE and Income Margin.

Investment thesis

I believe Robinhood’s popularity and extremely user-friendly platform will allow the company to keep expanding by reaching more and more “wannabe investors” both in the US and internationally.

I classify Robinhood as a low-cost provider. For this reason, I expect its net income margin to settle between Charles Schwab and IBKR at around 15% from year 3.

I expect a growth rate of 25% for the next 5 years thanks to its international expansion, which will linearly slow down to 2% in the terminal year.

The combination of high growth rate and average margins will allow Robinhood to deliver an ROE of around 15% from year 5 onwards, matching its direct competitors and the industry.

Robinhood valuation

Since Robinhood is a financial firm, the standard discounted cash flow method isn’t the best model to use. The reasons lie in the different uses of debt, which is more like a raw material than a standard liability, and financial companies’ reinvesting needs.

Following the academic paper “Valuing Financial Service firm” (A. Damodaran 2009), instead of a DCF, I valued Robinhood using the excess return model.

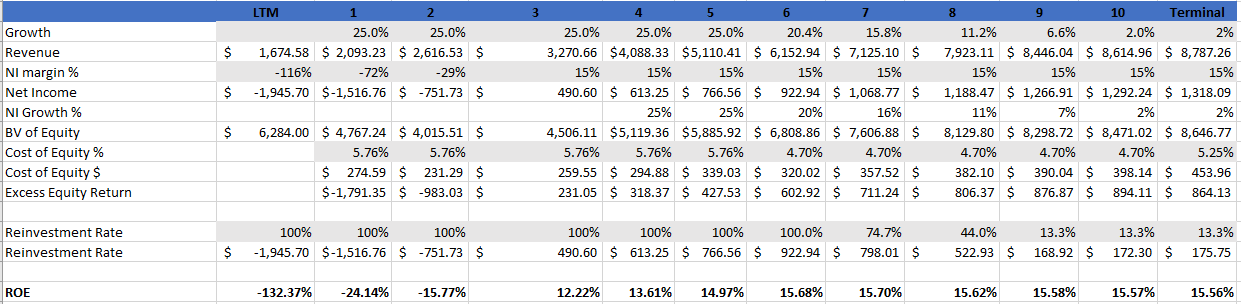

The inputs are explained in the paragraph “investment thesis” and are highlighted in grey in the table below. (See footnotes1 for more details)

By adding the present value of the future excess return to the current BV of equity, I get a fair value per share of $ 27.06, 44% below the current price.

Definetely not a stock to buy right now.

Risks involved

The biggest risk on Robinhood’s future is regulation risk. Will the company be able to keep its main revenue stream in the future? After all the drama surrounding the Payments for Order Flow, dark pools, and the probable review by the SEC, it’s not 100% sure that their commission-free business will be able to continue forever.

Secondly, in some countries like the UK the PFOF is illegal. Hence, Robinhood will need to find additional ways to generate revenue and still be appealing to its international clients. In Europe there are already plenty of brokers with little or zero commissions, will Robinhood be able to get their clients?

The good news is that I don’t see Robinhood going bankrupt or in any serious financial trouble in the medium term. The brand is strong and, in case they fail to become profitable, they will definitely be acquired by some other big players.

Conclusion

As expected, Robinhood is overvalued and there are many risks that could drive its valuation even lower. I’m definitely not buying it and, even if it falls below 27$, I would wait for a huge discount before buying it.

Before taking any investment decision on Robinhood, I would like to see first what are their expansion plans and how they plan to make money outside the US, and what the SEC will say about PFOF.

Invest for the long term and buy only when the stocks are cheap!

Subscribe & Share the article 👇

1) Altough the book value of equity is negative in the last report, after the IPO all the preferred convertible shares and convertible notes converted to common equity. Hence, I considered them as common equity. I also added the 900m of IPO proceeds, the $ 1bn left has been excluded since they it has been used to cover the cost of stock options.

2) The model implies no further secondary equity issuance with the any reinvestment need covered by retained earning and debt.

3) the equity value doesn’t include the value of the outstanding stock options since they don’t disclose how much options are left after the IPO. Hence the fair value may be biased on the upward.