Tesla (TSLA): Why Buying Bitcoin Decreased Its Fair Value

Full fundamental analysis and intrinsic valuation of Tesla (TSLA).

Subscribe to get a new exclusive intrinsic valuation every month!

Sign up now to get the next one straight to your inbox. 👇

DISCLAIMER: The publication expresses my own opinions. Information presented is for educational purposes ONLY and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies.

Introduction

For one full week, the hottest news in every financial website was:

“Tesla buys $1.5 billion in Bitcoin, plans to accept it as payment.”

Source:cnbc.com

In this article, I will first evaluate Tesla using a Discounted Cash Flow model and, secondly, analyse how this purchase could, directly and indirectly, affects the company and its shareholders.

TESLA: a financial overview

Let’s start by checking out what is the current financial situation at Tesla.

Horizontal analysis: Tesla vs its own history

After a drop in 2019, Revenues start to take off again, with an expected growth rate of 52% in 2021.

Gross profit margins came back to the 20+% range.

EBIT margins, Return on Invested Capital and Sales to Invested Capital improved each of the previous 4 years, and they are expected to continue their positive trend in FY 2021 as well.

The economy of scale is kicking off at Tesla, and I can see the results in the returns and efficiency measures.

How Tesla is performing against the automobile industry

Tesla has a market share of only 1.42% but is already at the top of the automobile industry in terms of efficiency and returns.

I listed all the 129 public automobile companies worldwide, and I divided their ratios into quartile and percentile, highlighting in red the one where Tesla is.

Quartile:

Percentile:

Tesla is already in the third quartile and on the top percentiles for all the three performance ratios I consider:

EBIT Margin

Return on Invested Capital (ROIC)

Sales to Invested Capital (Sales to IC)

I would say an excellent result for Elon Musk. 👇👇

How much are Tesla (TSLA) shares worth?

Before getting to how much the purchase of bitcoin has changed the intrinsic value of Tesla, we need to value the company first.

The financial model I’ll use is the common discounted cash flow, which I consider the best method to get a company's intrinsic value.

Discounted cash flow valuation of Tesla: key assumptions

To get a final intrinsic value, several assumptions need to be made.

To keep the estimations as realistic as possible, I use the industry quartiles and percentiles, market-implied Equity Risk Premium, and the sector's unlevered beta.

Key assumptions:

1] Market Share of 13% by 2030 = $ 300bn revenue = 40% CAGR year 1 to 5.

Tesla is a strong brand. It could be considered the Apple of the automobile sector.

This is mainly due to the success of Elon Musk as an entrepreneur, storyteller and public figure.

I expect its popularity to rise while its cars' price becomes more accessible to the wide population.

The strongest players in the industry are Volkswagen and Toyota, which get around 13% of the market share each.

I assume Tesla will be at the top there by 2030, with a market share of around 13%.

With an expected Total Addressable Market of $ 2.700bn in 2030, Tesla’s revenue will be around $ 350bn. ($ 2700bn * 13%)

2] Earnings before interests and taxes (EBIT) Margin: 11%

Tesla doesn’t only offer the car itself but the “Tesla experience” powered by the additional technology it includes in its models (Self-driving technology, etc.).

These additional technologies allow Tesla to sell its vehicles at a higher margin because the marginal cost of software is almost zero. In addition, once the software is developed, it costs nothing to deploy it on the existing cars.

For the above reasons, I expect Tesla to get an EBIT margin at the top of the 9th percentile: 11% EBIT Margin.

Why not above 11%? Because even if Tesla could sell its cars at a higher price, to reach the wider public, they need to consider the tradeoff between price (margin) and quantity sold (downward sloping demand curve).

3] Sales to invested capital: 3.8

With the current Sales to IC of 2.72, they are already at the top of the industry in terms of efficiency.

I expect Tesla to keep increasing its efficiency thanks to the Giga Factories and brand awareness. Therefore, I assume it reaches a Sales to Invested Capital ratio of 3.8 in all the new projects starting from year 1.

With a Sales to IC of 3.8 and an increasing EBIT Margin, Tesla will be delivering a Return on Invested Capital of around 30% between year 1 and 10.

4] Cost of capital.

I computed the cost of capital based on the following assumptions:

Stable debt to equity ratio of 20%.

A beta of 1.50 in year 1 to 5, and 1 thereafter.

An Equity Risk Premium of 5%.

Default spread starting at 1.91% and decreasing to 0.90% of the AAA-rated companies.

WACC cost of capital for Tesla:

Tesla intrinsic valuation

Now that we have all the assumption here how they play out in the next 10 years:

Chart:

The ROIC will peak at 35% in year 6 and decrease to 10% in the terminal year.

In the long run, every company's competitive advantage and excess returns will be eaten out by competition. Hence the ROIC in the terminal year can’t be too far from the cost of capital.

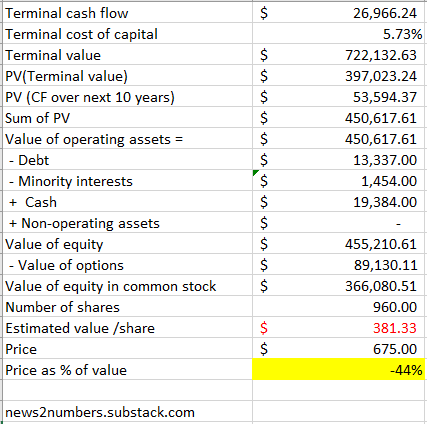

The fair value of Tesla shares:

Summing up the present value of all the future cash flows, taking out debt and minority interest, and adding cash, we get a fair value for the Tesla shares of 381$.

381$ per share is 44% lower than the market value of 675$ as of today. This means that Tesla is overvalued.

The value added by future growth is over 91% of the intrinsic value. This explains the high multiples Tesla is trading at.

Are you enjoying the article? Please subscribe 👇

What does the market expect from Tesla?

Now that we have seen the discounted cash flow based on my assumptions, let’s do some reverse engineering and let’s see what the market is expecting Tesla to do:

How much revenue is the market expecting Tesla to make in 10 years time?

I will keep some of the inputs constants and use the Goal Seek function in Excel to answer these questions.

Tesla expected revenues in 2030

By keeping constant all the assumptions minus the revenues in 2030, I run the goal seek function to see how big the market expects Tesla’s sales to be in 10 years.

By reverse-engineering the current stock price, we can see that the market expects Tesla to have $ 630bn revenue in year 10.

With an expected market size of $2700 bn, this implies a market share for Tesla of 23%.

Tesla Market-implied EBIT margin

If we assume that Tesla cannot reach a market share above the base assumption of 13%, the other variable that could explain the current stock price is a high EBIT margin.

The EBIT margin represents how much Tesla gets after paying all the expenses (except for Interests and Taxes).

This ratio is more related to the brand than the market share. If I have a strong brand, the customers will be happy to pay more and more as it's happening with Apple's products.

Keeping constant all the assumptions minus the EBIT Margin, I get that the market expects it to reach 19% by year 5.

Why is it important to get the implicit market expectations?

This exercise allows us to:

See what the market is expecting and decide if we agree or not;

Use the market expectations as a starting point for the “news to numbers conversion” I make in this newsletter.

As explained in my first article here, the goal of my publications is to translate financial news into updated intrinsic valuation models.

To update the models, I need to get a valuation first and then change it according to the news.

If I base the “news to numbers” analysis on my own previous inputs, I’ll make a series of double assumptions: how was the fair price before the news (first assumption) and how the news affected the intrinsic value (second assumption).

For example, the first assumption would have been “how much will be the market share of Tesla in 2030? (10%? 15%?)” and, on top of it, I would have made a second assumption “How much will it be influenced by the news? (10% decrease? 10% increase?”). Thus, I would lose one “degree of freedom”.

On the other side, if I use the market expectations as a starting point, I will make only one assumption (the effect on the market share after the news), and the analysis will be more precise.

How Tesla's purchase of Bitcoin changed its fair value?

The $1.5 bn investment in Bitcoin could influence the price in two ways:

Direct effect: increased beta, lower enterprise value, higher risk.

Indirect effect: Elon Musk publicly exposes himself to a controversial asset class (cryptocurrencies), affecting his reputation.

The direct effects of Tesla’s purchase of Bitcoin

1] Bitcoin doesn't produce any cash flow

To create added value for the shareholders, every investment made by a company should earn a return on investment (ROI) higher than the cost of capital.

Elon Musk has decided to spend his cash on $1.5 bn Bitcoin. Hence, the investment now has to deliver at least 7% a year to create additional value.

As we saw from the Discounted Cash Flow valuation above, to get the intrinsic value of a company, we need to:

Sum up the present value of the future cash flows.

Take out the debt.

Add the cash the company currently has.

Since Elon Musk used the company’s cash to buy Bitcoins and don’t produce any cash, the first direct effect of the investment is a decrease in the equity value of 1.5bn.

With 960m shares outstanding, the purchase automatically decreased Tesla’s value per share by $ 1.50.

2] Tesla is not a hedge fund

It’s not normal for an automobile company to invest in unregulated assets. This only adds complexity to the company, and hence it increases its risk.

In the last Tesla’s 10k, it’s clearly written:

We hold and may acquire digital assets that may be subject to volatile market prices, impairmen and unique risks of loss.

Everything that adds risk to the company decreases its value. 👇👇

Indirect effects of Tesla’s purchase of Bitcoin

By endorsing and advertising unregulated and controversial assets like Bitcoin and Dogecoin, Elon Musk exposes his reputation to a huge risk.

When an asset class is supported mainly by emotional, uninformed retail investors, the probabilities of it being a market bubble are high.

Once the bubble pops, many scams will be uncovered, a lot of investigations will start, and Elon Musk will find himself in the middle of the storm.

And, apparently, the storm is starting:

How does the reputation of Elon Musk affect Tesla?

As I wrote above, Tesla’s brand success is strictly linked to the public figure of Elon Musk. So when his reputation is hit, the brand of Tesla will be hit as well.

As stated on page 20 of Tesla’s 10k:

We are highly dependent on the services of Elon Musk, our Chief Executive Officer and largest stockholder. Although Mr Musk spends significant time with Tesla and is highly active in our management, he does not devote his full time and attention to Tesla.

A decrease in the brand’s value could have two direct effects:

1] A decrease in market share.

Customers will look elsewhere to buy an electric car because they don’t like the new company reputation.

Here the effects of a 10%, 25% and 50% decrease in Tesla’s revenues in 2030, starting from the implicit market share of 23% ($ 625bn revenues) calculated before.

2] A lower EBIT margin

Since the reputation has been hit, Tesla won’t be able to sell its cars at a premium price, and the EBIT margin will decrease.

The table above shows the effects of a possible decrease in the EBIT margin on the intrinsic share price.

Conclusion

As we have seen in this article, one small investment and one single financial news could have a big impact on a share price.

If you have any question or you want to suggest a company or news for the next article, leave a comment below or contact me on Twitter: @SanguaniniM

If you want to read the next News to Numbers’ analysis, subscribe and receive the next one straight in your inbox. 👇👇